Understanding Alternative Business Lending

Find Out How Much Cash Your Business Could Receive

The Smart Small Business Funding Solution

Small business owners in nearly every industry often face a similar financial challenge: securing additional capital for their business in a timely manner. Alternative business lenders are another financing option for small businesses who need to obtain funding. Banks have traditionally served small businesses as the primary outlet for acquiring financing. While banks have lengthy applications and take weeks or even months to approve loans, an alternative lender fills the gap for efficient financing solutions. An alternative lender provides loans, lines of credit, or cash advances to small businesses, outside of the traditional forms of credit offered by a bank, credit union, or the Small Business Administration (SBA).What is Alternative Business Lending?

Alternative business lending is a way for businesses to borrow money without going through a traditional financial institution. Instead of applying for a loan with a bank, business borrowers apply for financing through online alternative lenders, without having to visit a physical location. Alternative lenders are private financial companies that don’t have the same strict requirements that many banks do. Alternative lenders have less red tape to work through, making it an easier route to acquiring funding.

Many small businesses need access to additional capital. In 2019, over 43% of small businesses applied for a loan, according to the Federal Reserve Small Business Credit Survey. But as many small business owners can attest, obtaining a loan from a traditional bank isn’t always easy. This has helped pave the way for alternative business funding solutions.

Aside from the magnitude of paperwork required to apply, small business owners often lack the business history, healthy FICO score, and positive cash flow needed for approval. In recent years, banks have grown even more restrictive with their lending practices for fear of yet another economic downturn. In fact, according to Biz2Credit Small Business Lending Index, large financial institutions have an average loan approval rating of 14% as of February 2023.

To make matters even more challenging, banks are reluctant to relax loan requirements for small businesses and often consider small business loans too risky, favoring large businesses instead. A study from Harvard Business School found that since the recession, loans have increased 4 percent for large businesses but decreased 20 percent for small businesses. Luckily, alternative business lending has begun to change the way companies access business loans. As a result, small and medium-sized businesses that may not have qualified for a bank loan now have a way to get the capital they need through alternative business lending.

Traditional Banks vs. Alternative Business Lenders

Credit Qualifications

Loan Amounts

Funding Timeline

Revenue Requirements

How to Apply for an Alternative Business Loan?

Applying for alternative business financing is simple. While traditional banks have difficult and long application processes, alternative business lenders like QuickBridge limit the number of hoops you have to jump through. We believe securing a financing solution for your business should be as easy as possible.

Simply Apply Online

The application process is easy and only requires a driver’s license and bank statements.

Get a Quick Credit Decision

We provide fast credit decisions and offer flexible payment options that best fit your specific needs.

Receive Funds Fast

If a credit approval is established, funds are sent directly to your bank account in matter of days.

Popular Types of Alternative Business Loans

There are many loan types to suit every business need. At QuickBridge, one of our dedicated funding specialists works with you to tailor the right loan type to your unique needs. While a loan can be customized individually, there are many different loan types to consider when determining how a loan can help you achieve your business goals. Here are some of the most popular loan types you’ll find with alternative lenders:

Working Capital

This loan type is designed for everyday expenses and give businesses access to working capital for operational costs or growth opportunities. Working capital loans are intended for short-term expenses and typically have shorter repayment terms than other loan types. This is best suited for businesses who experience cash flow disruptions and need additional funding to cover daily expenses.

Short Term Business Loan

Short-term business loans are best suited for short-term needs as this loan type typically has a short repayment period, often 18 months or less. Instead of planning for long-term business growth, a short-term business loan supports businesses who need to make immediate inventory purchases or capitalize on an opportunity to acquire businesses.

Business Bridge Loans

A bridge loan for business is a loan intended to cover a specific purchase and help bridge the gap in payment when funds may not be yet available. This loan type helps businesses who need funds to pay for an inventory purchase or cover a lease payment.

Your Path to Business Funding Starts Here

Get fast financing for your business when you need it the most, not when the bank decides you're ready. Applying requires no commitment and takes just minutes to complete.

The Advantages of Using Alternative Business Lenders

Strict requirements often exclude small and new businesses from traditional bank loans. Business owners are discovering why an alternative lender is the best way to secure a financing solution for their business. Since the COVID-19 pandemic, loan approval ratings dropped significantly and are struggling to recover.

In 2022, big banks had a 14% approval rating compared to a 28% approval rating just two years ago, according to Forbes. Alternative lending fills the gap left by traditional banks for small businesses who find themselves unable to secure traditional financing. In 2019, for example, more than $15 billion was financed via online lenders, according to the Cambridge Centre for Alternative Finance. That’s more than all the previous years combined.

But why? Here are a handful of reasons alternative business lending is the new preferred option for small business owners:

Easier approval: Alternative lenders are easier to obtain due to their eligibility requirements. With less requirements, many businesses are more likely to get approved. Faster approval window: Instead of wait times lasting months, online lenders have approval times that are much shorter – often within 24 hours or less.

Faster approval window: Instead of wait times lasting months, online lenders have approval times that are much shorter – often within 24 hours or less.

Enhanced flexibility: Alternative lenders can offer different loan terms and repayment options than banks.

Various loan types: Online lenders offer a variety of financing solutions that big banks lack, and work with business owners to customize the right loan option.

Less paperwork: Alternative lenders typically require less financial documents and business information from small business owners.

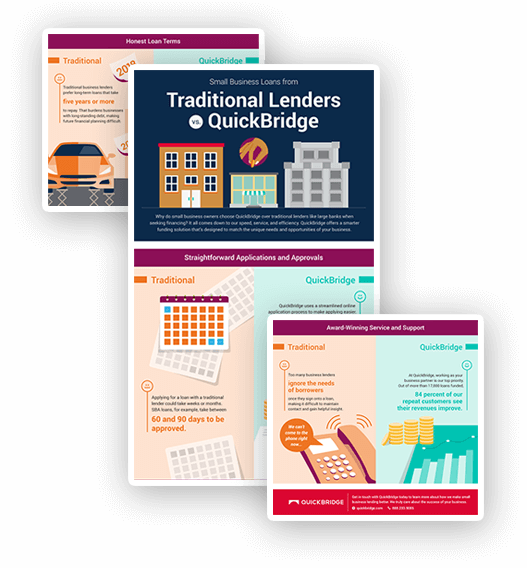

Traditional Loans vs. QuickBridge

Comparison Infographic

Why do thousands of small business owners choose QuickBridge over traditional lenders when seeking financing? It all comes down to our speed, service level and expertise. View the Infographic

When to Consider an Alternative Lender

Alternative funding is a flexible financing solution, but when should a small business consider applying with an alternative lender? If you were recently denied financing from a traditional bank, you should consider applying through an alternative lender as the approval rate generally tends to be higher.

There are many other ways to tell if the timing is right for your small business to apply for funding – whether you want to bridge gaps in funding or capitalize on an investment opportunity.

You may want to consider applying for alternative financing if you:

- • Have been in business for at least six months

- • Need access to immediate funds

- • Were recently denied funding through a traditional bank

- • Can making weekly or monthly repayments

- • Need a smaller loan amount

- • Have cash flow disruptions or shortages

Alternative lenders typically require $250,000 in annual revenue, at least six months in business, and fair to excellent credit. If your business meets that criteria and is experiencing cash flow issues, unexpected expenses, or growth opportunities, then the timing may be right for you to apply for alternative financing.

Why QuickBridge for Alternative Lending?

There’s a lot of options to choose from – so why work with QuickBridge? We’re dedicated to helping small businesses thrive. In fact, QuickBridge started as a small business and prides itself on supporting small businesses nationwide. Our team of dedicated funding specialists are consistently rated among the top in the industry and work closely with our customers to find them the best loan to suit their needs.

Alternative Financing Resources

Why Small Business Owners Should Seek Alternative Lending

Alternative lending fills in the gap left by traditional lenders by offering a quick and efficient approach to financing solutions. Alternative lenders are increasingly growing in popularity as Americans navigate through a period of high inflation.

Traditional vs. Alternative Lenders White Paper Guide

There are some major differences in how alternative lenders operate compared to traditional banks. Learn the differences between traditional and alternative lenders by downloading our in-depth, FREE white paper.